Kenny Dettman comes from a 15-year background of working as a global tax expert, CEO, Founder, and Operator. He previously worked as a Managing Director at Alvarez & Marsal.

More recently, he founded and led EZ-ERC who is an industry expert and pioneer within the Employee Retention Tax Credits. Kenny is a member of the Forbes Business Council and has been published in the Wall Street Journal.

Frank Tumminello

Frank Tumminello comes from a decade-long background of working in the financial services and technology industry. Prior to FileForms, he was an investor, acquirer, and value-creation resource in several financial services, insurance, and healthcare businesses throughout his private equity, corporate development, and investment banking career.

Frank began his career at Raymond James, followed by Oppenheimer & Co. and Century Equity Partners. Most recently, he led a pre-tax healthcare benefits third-party administrator through eight successful acquisitions and a majority recapitalization with a multi-billion-dollar private equity firm. Frank holds his Bachelor of Science in Physics from Bates College, where he minored in Mathematics and wrote a year-long thesis in Computer Science.

About FileForms

FileForms is the trusted software partner for filing federal and state forms and reports on behalf of businesses and their advisors. Its flagship product is a reporting solution for the Beneficial Ownership Information (BOI) report, a new federal filing requirement resulting from the Corporate Transparency Act (CTA) that is enforced by the Financial Crimes Enforcement Network (FinCEN), expected to impact more than 35 million U.S. businesses.

The FileForms team is unwaveringly dedicated to revolutionizing the process of preparing and submitting the growing number of federal and state reporting obligations, such as the BOI report, which extend beyond traditional IRS and state tax filings. FileForms had developed a cutting-edge technology platform led by its accomplished executive team to holistically bring ease and accuracy to the compliance requirements of businesses and their advisors.

The Unauthorized Practice of Law and the Corporate Transparency Act

By FileForms | December 28, 2023

The Corporate Transparency Act (CTA) was enacted in 2021 to mitigate illicit financial activities by requiring most companies that conduct business in the U.S. to report specific information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN).

FinCEN is a bureau of the U.S. Treasury whose mission is to combat financial crimes by collecting and analyzing information about financial transactions to combat money laundering, terrorist financing, and other financial crimes. The CTA’s reporting requirements take effect on January 1, 2024, and the implications for U.S. business owners and their professional service providers are far-reaching.

Beneficial Ownership Information (BOI) Reporting

Unbeknownst to most business owners and even their trusted advisors, BOI reporting is a novel informational filing that will impact approximately 36 – 40 million businesses in the U.S. Certain companies formed before January 1, 2024, who do not qualify for an exemption must file their initial report by January 1, 2025.

New companies formed after January 1, 2024, only have 90 days from formation to file their initial BOI report. Time is of the essence, and U.S. business owners will undoubtedly turn to their professional service providers for guidance and assistance with this new filing requirement. It’s imperative for business advisors to understand their responsibilities and limitations in assisting their clients with CTA compliance.

While BOI reporting may be viewed as a tax filing, it is not administered by the Internal Revenue Service (IRS) and is subject to different rules and regulations. One of the most essential concepts for nonlawyer professional service providers to be aware of is the Unauthorized Practice of Law (UPL).

The UPL rules dictate what services nonlawyers such as CPAs, tax professionals, and registered agents may provide their clients. Any nonlawyer engaging in UPL may be subject to civil penalties, including fines, loss of licensure, or the ability to practice. Further, nonlawyers cannot collect professional fees directly from their clients for providing such services.

Depending on the severity of UPL violations, practitioners may even be subject to criminal penalties, including jail time.

What is UPL?

The premise of UPL rules is to protect consumers and ensure that practitioners render competent and ethical legal advice aligned with their clients’ interests. However, the Courts have issued many vague opinions over the years that have not concisely defined the practice of law. To determine whether a nonlawyer professional has engaged in UPL, courts have applied tests focusing on the following:

The difficulty of the services rendered;

Whether such services are incidental in form; or,

The services impact on the recipient’s legal rights.

This is intended to provide an overview of the UPL rules and their implications for practitioners. A detailed discussion of the various Courts’ interpretations of UPL over the years is beyond the scope of this article. However, professional service providers should be aware that the UPL rules are complex and vary in each jurisdiction[1].

While some states hold that the practice of law is anything that lawyers do,[2] others merely list activities that constitute the practice of law.[3] Due to the differing views of the States and federal laws that don’t provide a concise definition of UPL, nonlawyers must frequently collaborate with the appropriate legal professionals to ensure they do not inadvertently engage in UPL.

Multidisciplinary Practices (MDPs)

Professional service firms that offer their clients a wide array of professional services are referred to as multidisciplinary practices. Such practices may employ various professionals, including but not limited to lawyers, accountants, registered agents, and financial advisors. Each of these professionals must understand their roles, responsibilities, and especially the limitations of the services they provide their clients.

CPAs, in particular, enjoy certain freedoms due to their strict licensing requirements that encourage competent and ethical practices by licensed CPAs and the staff accountants who assist them. CPAs who pass an additional test may even represent their clients in the U.S. Tax Court.

However, CPAs must still be wary of crossing the line and providing legal advice to their clients. When in doubt, it would be prudent for CPAs to consult or collaborate with an attorney.

Application of UPL to the Corporate Transparency Act

The complexity of a BOI report will vary greatly depending on the nature of the client’s structure and industry. Consider a simple example: a small pizza shop organized as a single-member limited liability company (LLC) in Florida with only three employees and $250,000 in annual revenue. The business owner’s CPA could easily determine that the business does not qualify for an exemption and may collect the necessary information and file the BOI report on behalf of the business. This would be well within the CPA’s capabilities and would not be considered UPL.

However, if a private equity firm engages a CPA to prepare the BOI reports for hundreds of portfolio companies operating in various industries, this requires substantial analysis and a deep understanding of the CTA and the associated regulations. If a nonlawyer CPA were to perform this analysis independently and file the BOI reports without consulting a legal professional, they could be deemed to be engaging in UPL.

Accordingly, nonlawyer professional service providers should engage a qualified legal professional to assist with the more complex nuances of the CTA and BOI reporting.

Key Takeaways

Nonlawyer professional service providers must be wary of inadvertently engaging in UPL. As the complexity of an engagement increases, it would be wise for these professionals to consult with an attorney to ensure they do not expose themselves and their clients to unnecessary risk by performing analyses and making determinations that require the requisite legal knowledge of a licensed attorney.

The consequences for nonlawyer professionals engaging in UPL extend not only to civil and criminal penalties but also damage to their professional reputations. Clients depend on their trusted advisors to guide them through complex problems, whether they be financial, legal, or a multitude of issues.

How FileForms Can Help

FileForms team of CPAs and attorneys mitigates professional service providers’ risk of engaging in UPL by employing tax and legal industry experts with the requisite knowledge to properly handle their Clients’ BOI reporting needs.

Whether these providers want to handle their clients’ BOI reports in-house or outsource their BOI function to FileForms team, solutions are available for every instance. For more information, please visit our website or contact us.

[1] The ABA Model Rules do not attempt to define the practice of law. MODEL RULES OF PROF’L CONDUCT R. 5.5 cmt. (2011) (“The definition of the practice of law is established by law and varies from one jurisdiction to another.”).

[2] See Gary G. Sackett, An Analytic Approach to Defining the “Practice of Law” Utah’s New Definition, UTAH B.J., Jan. 20, 2006, http://webster.utahbar.orgIbarjoumal/2006/01/ananalyticapproachtodefini.html (explaining that most legislatures, courts, bar associations, and committees’ attempts to define the practice of law are “circular because they define a concept in terms of the very term ‘law’ or its derivatives such as ‘lawyer’ and ‘legal.’).

[3] Melone, supra note 10, at 53; see also Ronald A. Landen, Comment, The Prospects of the Accountant-Lawyer Multidisciplinary Partnership in English-Speaking Countries, 13 EMORY INT’L L. REV. 763, 774-90 (1999) (providing descriptions of how various U.S. and international jurisdictions define the practice of law.

Beneficial Ownership Information Reporting

Frequently Asked Questions

FinCEN has prepared the following Frequently Asked Questions (FAQs) in response to inquiries received relating to the Beneficial Ownership Information Reporting Rule.

These FAQs are explanatory only and do not supplement or modify any obligations imposed by statute or regulation. Please refer to the Beneficial Ownership Information Reporting Rule, available at www.fincen.gov/boi, for details on specific provisions. FinCEN expects to publish additional guidance in the future. Questions may be submitted on FinCEN’s Contact web page.

A. 2. Why do companies have to report beneficial ownership information to the U.S. Department of the Treasury?

In 2021, Congress passed the Corporate Transparency Act on a bipartisan basis. This law creates a new beneficial ownership information reporting requirement as part of the U.S. government’s efforts to make it harder for bad actors to hide or benefit from their ill-gotten gains through shell companies or other opaque ownership structures.

A. 3. Under the Corporate Transparency Act, who can access beneficial ownership information?

FinCEN will permit Federal, State, local, and Tribal officials, as well as certain foreign officials who submit a request through a U.S. Federal government agency, to obtain beneficial ownership information for authorized activities related to national security, intelligence, and law enforcement. Financial institutions will have access to beneficial ownership information in certain circumstances, with the consent of the reporting company. Those financial institutions’ regulators will also have access to beneficial ownership information when they supervise the financial institutions.

FinCEN published the rule that will govern access to and protection of beneficial ownership information on December 22, 2023. Beneficial ownership information reported to FinCEN will be stored in a secure, non-public database using rigorous information security methods and controls typically used in the Federal government to protect non-classified yet sensitive information systems at the highest security level. FinCEN will work closely with those authorized to access beneficial ownership information to ensure that they understand their roles and responsibilities in using the reported information only for authorized purposes and handling in a way that protects its security and confidentiality.

A. 4. How will companies become aware of the BOI reporting requirements?

FinCEN is engaged in a robust outreach and education campaign to raise awareness of and help reporting companies understand the new reporting requirements. That campaign involves virtual and in-person outreach events and comprehensive guidance in a variety of formats and languages, including multimedia content and the Small Entity Compliance Guide, as well as new channels of communication, including social media platforms. FinCEN is also engaging with governmental offices at the federal and state levels, small business and trade associations, and interest groups.

FinCEN will continue to provide guidance, information, and updates related to the BOI reporting requirements on its BOI webpage, www.fincen.gov/boi. Subscribe here to receive updates via email from FinCEN about BOI reporting obligations.

B. 1. Should my company report beneficial ownership information now?

FinCEN launched the BOI E-Filing website for reporting beneficial ownership information (https://boiefiling.fincen.gov) on January 1, 2024.

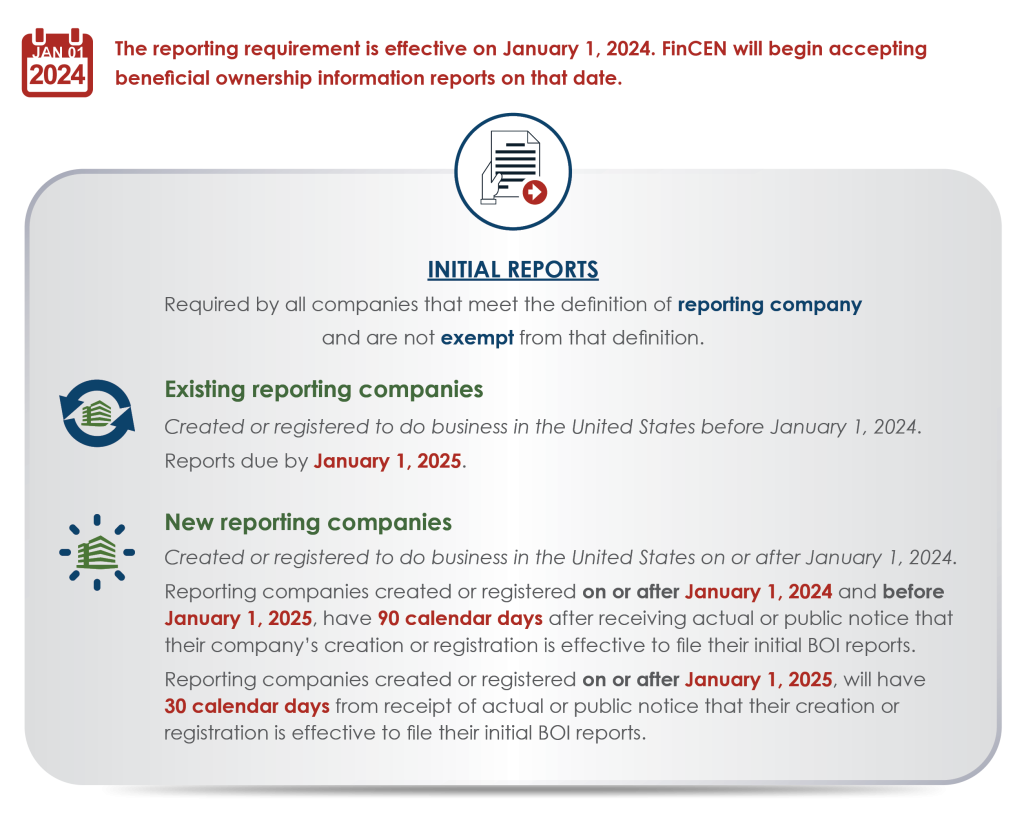

A reporting company created or registered to do business before January 1, 2024, will have until January 1, 2025, to file its initial BOI report.

A reporting company created or registered in 2024 will have 90 calendar days to file after receiving actual or public notice that its creation or registration is effective.

A reporting company created or registered on or after January 1, 2025, will have 30 calendar days to file after receiving actual or public notice that its creation or registration is effective.

B. 2. When do I need to report my company’s beneficial ownership information to FinCEN?

A reporting company created or registered to do business before January 1, 2024, will have until January 1, 2025 to file its initial beneficial ownership information report.

A reporting company created or registered on or after January 1, 2024, and before January 1, 2025, will have 90 calendar days after receiving notice of the company’s creation or registration to file its initial BOI report. This 90-calendar day deadline runs from the time the company receives actual notice that its creation or registration is effective, or after a secretary of state or similar office first provides public notice of its creation or registration, whichever is earlier.

Reporting companies created or registered on or after January 1, 2025, will have 30 calendar days from actual or public notice that the company’s creation or registration is effective to file their initial BOI reports with FinCEN.

B. 3. When will FinCEN accept beneficial ownership information reports?

FinCEN will begin accepting beneficial ownership information reports on January 1, 2024. Beneficial ownership information reports will not be accepted before then.

B. 5. How will I report my company’s beneficial ownership information?

If you are required to report your company’s beneficial ownership information to FinCEN, you will do so electronically through a secure filing system available via FinCEN’s BOI E-Filing website (https://boiefiling.fincen.gov).

B. 7. Is a reporting company required to use an attorney or a certified public accountant (CPA) to submit beneficial ownership information to FinCEN?

No. FinCEN expects that many, if not most, reporting companies will be able to submit their beneficial ownership information to FinCEN on their own using the guidance FinCEN has issued. Reporting companies that need help meeting their reporting obligations can consult with professional service providers such as lawyers or accountants.

B. 8. Who can file a BOI report on behalf of a reporting company, and what information will be collected on filers?

Anyone whom the reporting company authorizes to act on its behalf—such as an employee, owner, or third-party service provider—may file a BOI report on the reporting company’s behalf. When submitting the BOI report, individual filers should be prepared to provide basic contact information about themselves, including their name and email address or phone number.

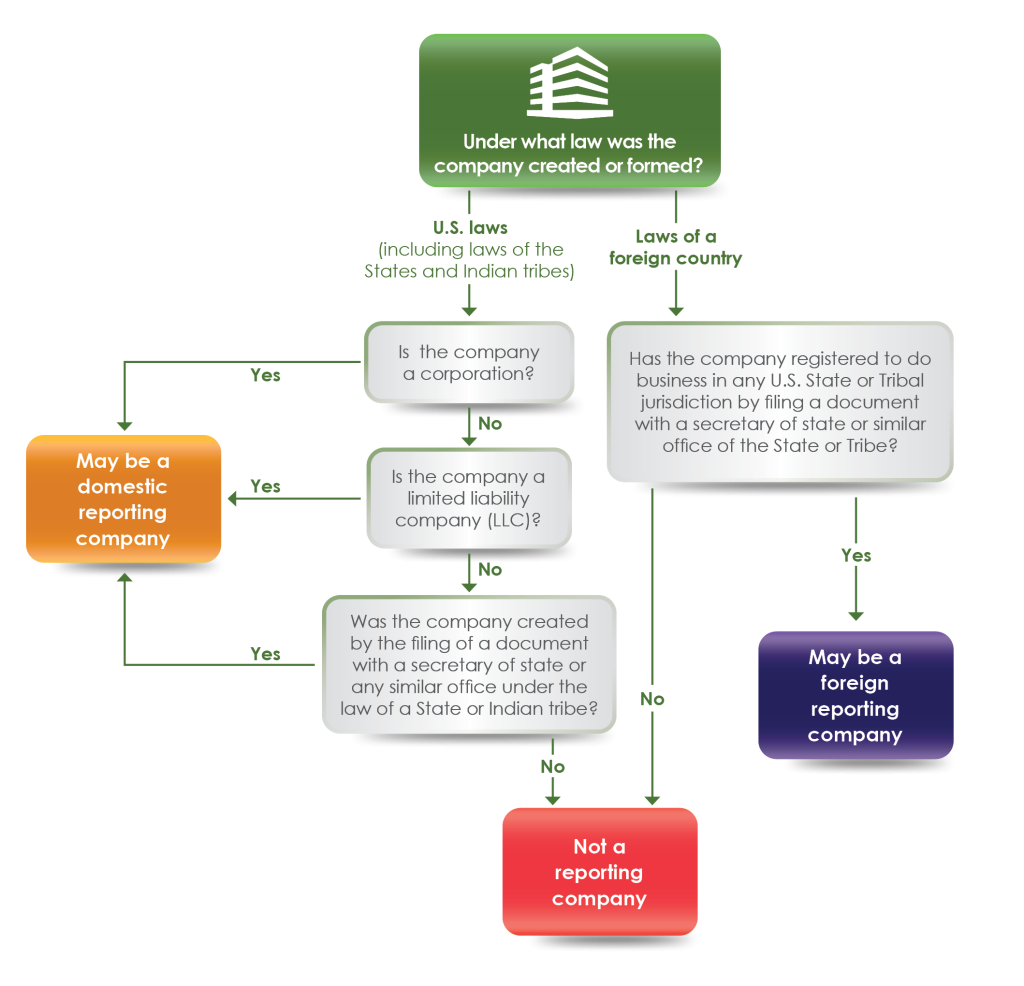

C. 1. What companies will be required to report beneficial ownership information to FinCEN?

Companies required to report are called reporting companies. There are two types of reporting companies:

Domestic reporting companies are corporations, limited liability companies, and any other entities created by the filing of a document with a secretary of state or any similar office in the United States.

Foreign reporting companies are entities (including corporations and limited liability companies) formed under the law of a foreign country that have registered to do business in the United States by the filing of a document with a secretary of state or any similar office.

There are 23 types of entities that are exempt from the reporting requirements (see Question C.2). Carefully review the qualifying criteria before concluding that your company is exempt.

FinCEN’s Small Entity Compliance Guide for beneficial ownership information reporting includes the following flowchart to help identify if a company is a reporting company (see Chapter 1.1, “Is my company a “reporting company”?”).

C. 2. Are some companies exempt from the reporting requirement?

Yes, 23 types of entities are exempt from the beneficial ownership information reporting requirements. These entities include publicly traded companies meeting specified requirements, many nonprofits, and certain large operating companies.

The following table summarizes the 23 exemptions:

Exemption No.

Exemption Short Title

1

Securities reporting issuer

2

Governmental authority

3

Bank

4

Credit union

5

Depository institution holding company

6

Money services business

7

Broker or dealer in securities

8

Securities exchange or clearing agency

9

Other Exchange Act registered entity

10

Investment company or investment adviser

11

Venture capital fund adviser

12

Insurance company

13

State-licensed insurance producer

14

Commodity Exchange Act registered entity

15

Accounting firm

16

Public utility

17

Financial market utility

18

Pooled investment vehicle

19

Tax-exempt entity

20

Entity assisting a tax-exempt entity

21

Large operating company

22

Subsidiary of certain exempt entities

23

Inactive entity

FinCEN’s Small Entity Compliance Guide includes this table and checklists for each of the 23 exemptions that may help determine whether a company meets an exemption (see Chapter 1.2, “Is my company exempt from the reporting requirements?”). Companies should carefully review the qualifying criteria before concluding that they are exempt. Please see additional FAQs about reporting company exemptions in “L. Reporting Company Exemptions” below.

C. 3. Are certain corporate entities, such as statutory trusts, business trusts, or foundations, reporting companies?

It depends. A domestic entity such as a statutory trust, business trust, or foundation is a reporting company only if it was created by the filing of a document with a secretary of state or similar office. Likewise, a foreign entity is a reporting company only if it filed a document with a secretary of state or a similar office to register to do business in the United States.

State laws vary on whether certain entity types, such as trusts, require the filing of a document with the secretary of state or similar office to be created or registered.

If a trust is created in a U.S. jurisdiction that requires such filing, then it is a reporting company, unless an exemption applies.

Similarly, not all states require foreign entities to register by filing a document with a secretary of state or a similar office to do business in the state.

However, if a foreign entity has to file a document with a secretary of state or a similar office to register to do business in a state, and does so, it is a reporting company, unless an exemption applies.

Entities should also consider if any exemptions to the reporting requirements apply to them. For example, a foundation may not be required to report beneficial ownership information to FinCEN if the foundation qualifies for the tax-exempt entity exemption.

Chapter 1 of FinCEN’s Small Entity Compliance Guide (“Does my company have to report its beneficial owners?”) may assist companies in identifying whether they need to report.

C. 4. Is a trust considered a reporting company if it registers with a court of law for the purpose of establishing the court’s jurisdiction over any disputes involving the trust?

No. The registration of a trust with a court of law merely to establish the court’s jurisdiction over any disputes involving the trust does not make the trust a reporting company.

C. 5. Does the activity or revenue of a company determine whether it is a reporting company?

Sometimes. A reporting company is (1) any corporation, limited liability company, or other similar entity that was created in the United States by the filing of a document with a secretary of state or similar office (in which case it is a domestic reporting company), or any legal entity that has been registered to do business in the United States by the filing of a document with a secretary of state or similar office (in which case it is a foreign reporting company), that (2) does not qualify for any of the exemptions provided under the Corporate Transparency Act. An entity’s activities and revenue, along with other factors in some cases, can qualify it for one of those exemptions. For example, there is an exemption for certain inactive entities, and another for any company that reported more than $5 million in gross receipts or sales in the previous year and satisfies other exemption criteria. Neither engaging solely in passive activities like holding rental properties, for example, nor being unprofitable necessarily exempts an entity from the BOI reporting requirements.

FinCEN’s Small Entity Compliance Guide provides additional information concerning exemptions in Chapter 1.2, “Is my company exempt from the reporting requirements?”

C. 6. Is a sole proprietorship a reporting company?

No, unless a sole proprietorship was created (or, if a foreign sole proprietorship, registered to do business) in the United States by filing a document with a secretary of state or similar office. An entity is a reporting company only if it was created (or, if a foreign company, registered to do business) in the United States by filing such a document. Filing a document with a government agency to obtain (1) an IRS employer identification number, (2) a fictitious business name, or (3) a professional or occupational license does not create a new entity, and therefore does not make a sole proprietorship filing such a document a reporting company.

C. 7. Can a company created or registered in a U.S. territory be considered a reporting company?

Yes. In addition to companies in the 50 states and the District of Columbia, a company that is created or registered to do business by the filing of a document with a U.S. territory’s secretary of state or similar office, and that does not qualify for any exemptions to the reporting requirements, is required to report beneficial ownership information to FinCEN. U.S. territories are the Commonwealth of Puerto Rico, the Commonwealth of the Northern Mariana Islands, American Samoa, Guam, and the U.S. Virgin Islands.

D. 1. Who is a beneficial owner of a reporting company?

A beneficial owner is an individual who either directly or indirectly: (1) exercises substantial control (see Question D.2) over the reporting company, or (2) owns or controls at least 25% of the reporting company’s ownership interests (see Question D.4).

FinCEN’s Small Entity Compliance Guide provides checklists and examples that may assist in identifying beneficial owners (see Chapter 2.3 “What steps can I take to identify my company’s beneficial owners?”).

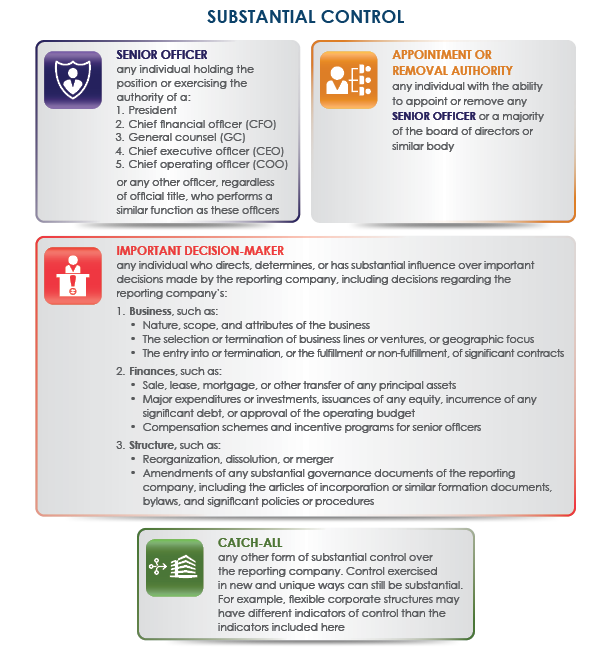

An individual can exercise substantial control over a reporting company in four different ways. If the individual falls into any of the categories below, the individual is exercising substantial control:

The individual is a senior officer (the company’s president, chief financial officer, general counsel, chief executive office, chief operating officer, or any other officer who performs a similar function).

The individual has authority to appoint or remove certain officers or a majority of directors (or similar body) of the reporting company.

The individual is an important decision-maker for the reporting company. See Question D.3 for more information.

The individual has any other form of substantial control over the reporting company as explained further in FinCEN’s Small Entity Compliance Guide (see Chapter 2.1, “What is substantial control?”).

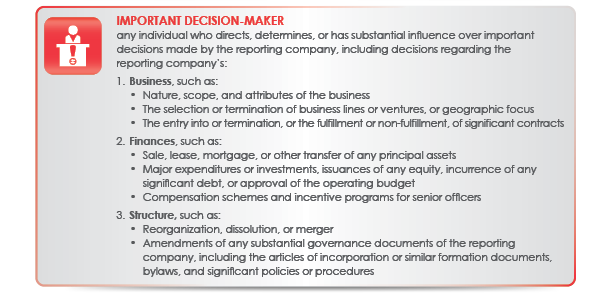

D. 3. One of the indicators of substantial control is that the individual is an important decision-maker. What are important decisions?

Important decisions include decisions about a reporting company’s business, finances, and structure. An individual that directs, determines, or has substantial influence over these important decisions exercises substantial control over a reporting company. Chapter 2.1, “What is substantial control?” of FinCEN’s Small Entity Compliance Guide provides the following information:

An ownership interest is generally an arrangement that establishes ownership rights in the reporting company. Examples of ownership interests include shares of equity, stock, voting rights, or any other mechanism used to establish ownership.

Chapter 2.2, “What is ownership interest?” of FinCEN’s Small Entity Compliance Guide discusses ownership interests and sets out steps to assist in determining the percentage of ownership interests held by an individual.

D. 5. Who qualifies for an exception from the beneficial owner definition?

There are five instances in which an individual who would otherwise be a beneficial owner of a reporting company qualifies for an exception. In those cases, the reporting company does not have to report that individual as a beneficial owner to FinCEN.

FinCEN’s Small Entity Compliance Guide includes a checklist to help determine whether any exceptions apply to individuals who might otherwise qualify as beneficial owners (see Chapter 2.4. “Who qualifies for an exception from the beneficial owner definition?”).

D. 6. Is my accountant or lawyer considered a beneficial owner?

Accountants and lawyers generally do not qualify as beneficial owners, but that may depend on the work being performed.

Accountants and lawyers who provide general accounting or legal services are not considered beneficial owners because ordinary, arms-length advisory or other third-party professional services to a reporting company are not considered to be “substantial control” (see Question D.2). In addition, a lawyer or accountant who is designated as an agent of the reporting company may qualify for the “nominee, intermediary, custodian, or agent” exception from the beneficial owner definition.

However, an individual who holds the position of general counsel in a reporting company is a “senior officer” of that company and is therefore a beneficial owner. FinCEN’s Small Entity Compliance Guide includes a checklist to help determine whether an individual qualifies for an exception to the beneficial owner definition (see Chapter 2.4, “Who qualifies for an exception from the beneficial owner definition?”).

D. 7. What information should a reporting company report about a beneficial owner who holds their ownership interests in the reporting company through multiple exempt entities?

If a beneficial owner owns or controls their ownership interests in a reporting company exclusively through multiple exempt entities, then the names of all of those exempt entities may be reported to FinCEN instead of the individual beneficial owner’s information.

Note that this special rule does not apply when an individual owns or controls ownership interests in a reporting company through both exempt and non-exempt entities. In that case, the reporting company must report the individual as a beneficial owner (if no exception applies), but the exempt companies do not need to be listed.

FinCEN’s Small Entity Compliance Guide includes more information about this special reporting rule in Chapter 4.2, “What do I report if a special reporting rule applies to my company?”

D. 8. Is an unaffiliated company that provides a service to the reporting company by managing its day-to-day operations, but does not make decisions on important matters, a beneficial owner of the reporting company?

The unaffiliated company itself cannot be a beneficial owner of the reporting company because a beneficial owner must be an individual. Any individuals that exercise substantial control over the reporting company through the unaffiliated company must be reported as beneficial owners of the reporting company. However, individuals who do not direct, determine, or have substantial influence over important decisions made by the reporting company, and do not otherwise exercise substantial control, may not be beneficial owners of the reporting company.

Please see Chapter 2.1 of FinCEN’s Small Entity Compliance Guide, “What is substantial control?” for additional information on how to determine whether an individual has substantial control over a reporting company.

D. 9. Is a member of a reporting company’s board of directors always a beneficial owner of the reporting company?

No. A beneficial owner of a company is any individual who, directly or indirectly, exercises substantial control over a reporting company, or who owns or controls at least 25 percent of the ownership interests of a reporting company.

Whether a particular director meets any of these criteria is a question that the reporting company must consider on a director-by-director basis.

FinCEN’s Small Entity Compliance Guide includes additional information on how to determine if an individual qualifies as a beneficial owner in Chapter 2, “Who is a beneficial owner of my company?”. This chapter includes separate sections with more information about substantial control and ownership interest: Chapter 2.1 “What is substantial control?” and Chapter 2.2 “What is ownership interest?”

D. 10. Is a reporting company’s designated “partnership representative” or “tax matters partner” a beneficial owner?

It depends. A reporting company’s “partnership representative,” as defined in 26 U.S.C. 6223, or “tax matters partner,” as the term was previously defined in now-repealed 26 U.S.C. 6231(a)(7), is not automatically a beneficial owner of the reporting company. However, such an individual may qualify as a beneficial owner of the reporting company if the individual exercises substantial control over the reporting company, or owns or controls at least 25 percent of the company’s ownership interests.

Chapter 2 of FinCEN’s Small Entity Compliance Guide (“Who is a beneficial owner of my company?”) has additional information on how to determine if an individual qualifies as a beneficial owner of a reporting company.

Note that a “partnership representative” or “tax matters partner” serving in the role of a designated agent of the reporting company may qualify for the “nominee, intermediary, custodian, or agent” exception from the beneficial owner definition.

FinCEN’s Small Entity Compliance Guide includes additional information on such exemptions in Chapter 2.4, “Who qualifies for an exception from the beneficial owner definition?”

D. 11. What should a reporting company report if its ownership is in dispute?

If ownership of a reporting company is the subject of active litigation and an initial BOI report has not been filed, a person authorized by the company to file its beneficial ownership information should comply with the requirements by reporting:

all individuals who exercise substantial control over the company, and

all individuals who own or control, or have a claim to ownership or control of, at least 25 percent ownership interests in the company.

If an initial BOI report has been filed, and if the resolution of the litigation leads to the reporting company having different beneficial owners from those reported (for example, because some individuals’ claims to ownership or control have been rejected), the reporting company must file an updated BOI report within 30 calendar days of resolution of the litigation.

D. 12. Who does a reporting company report as a beneficial owner if a corporate entity owns or controls 25 percent or more of the ownership interests of the reporting company?

Ordinarily, such a reporting company reports the individuals who indirectly either (1) exercise substantial control over the reporting company or (2) own or control at least 25 percent of the ownership interests in the reporting company through the corporate entity. It should not report the corporate entity that acts as an intermediate for the individuals.

For an example of how to calculate the percentage of ownership interests an individual owns or controls in a reporting company if the individual’s ownership interests are held through an intermediate entity, please review example 4 in Chapter 2.3, “What steps can I take to identify my company’s beneficial owners?” of FinCEN’s Small Entity Compliance Guide.

Two special rules create exceptions to this general rule in very specific circumstances:

A reporting company may report the name(s) of an exempt entity or entities in lieu of an individual beneficial owner who owns or controls ownership interests in the reporting company entirely through ownership interests in the exempt entity or entities; or

If the beneficial owners of the reporting company and the intermediate company are the same individuals, a reporting company may report the FinCEN identifier and full legal name of an intermediate company through which an individual is a beneficial owner of the reporting company.

FinCEN’s Small Entity Compliance Guide includes additional information about these special reporting rules (see Chapter 4.2, “What do I report if a special reporting rule applies to my company?”).

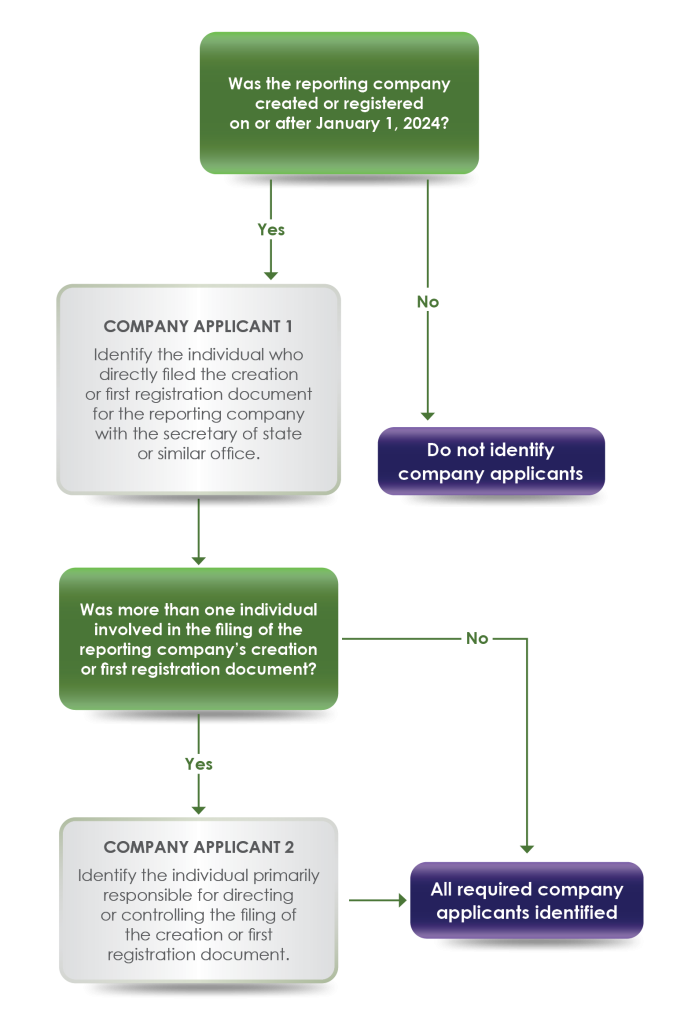

E. 1. Who is a company applicant of a reporting company?

Only reporting companies created or registered on or after January 1, 2024, will need to report their company applicants.

A company that must report its company applicants will have only up to two individuals who could qualify as company applicants:

The individual who directly files the document that creates or registers the company; and

If more than one person is involved in the filing, the individual who is primarily responsible for directing or controlling the filing.

The following flowchart can help identify the company applicant.

In addition, Chapter 3.2, “Who is a company applicant of my company?” of FinCEN’s Small Entity Compliance Guide includes additional information to help identify company applicants.

E. 2. Which reporting companies are required to report company applicants?

Not all reporting companies have to report their company applicants to FinCEN.

A reporting company must report its company applicants only if it is either a:

Domestic reporting company created in the United States on or after January 1, 2024; or

Foreign reporting company first registered to do business in the United States on or after January 1, 2024.

A reporting company does not have to report its company applicants if it is either a:

Domestic reporting company created in the United States before January 1, 2024; or

Foreign reporting company first registered to do business in the United States before January 1, 2024.

Below is summary of the company applicant reporting requirement. Chapter 3.1, “Is my company required to report its company applicants?” of FinCEN’s Small Entity Compliance Guide includes additional information.

E. 3. Is my accountant or lawyer considered a company applicant?

An accountant or lawyer could be a company applicant, depending on their role in filing the document that creates or registers a reporting company. In many cases, company applicants may work for a business formation service or law firm.

An accountant or lawyer may be a company applicant if they directly filed the document that created or registered the reporting company. If more than one person is involved in the filing of the creation or registration document, an accountant or lawyer may be a company applicant if they are primarily responsible for directing or controlling the filing.

For example, an attorney at a law firm that offers business formation services may be primarily responsible for overseeing preparation and filing of a reporting company’s incorporation documents. A paralegal at the law firm may directly file the incorporation documents at the attorney’s request. Under those circumstances, the attorney and the paralegal are both company applicants for the reporting company.

E. 4. Can a company applicant be removed from a BOI report if the company applicant no longer has a relationship with the reporting company?

No. A company applicant may not be removed from a BOI report even if the company applicant no longer has a relationship with the reporting company. A reporting company created on or after January 1, 2024, is required to report company applicant information in its initial BOI report, but is not required to file an updated BOI report if information about a company applicant changes.

E. 5. The company applicants of a reporting company include the individual “primarily responsible for directing the filing of the creation or registration document.” What makes an individual “primarily responsible” for directing such a filing?

At most, two individuals need to be reported as company applicants:

the person who directly files the document with a secretary of state or similar office, and

if more than one person is involved in the filing of the document, the person who is primarily responsible for directing or controlling the filing.

For the purposes of determining who is a company applicant, it is not relevant who signs the creation or registration document, for example, as an incorporator. To determine who is primarily responsible for directing or controlling the filing of the document, consider who is responsible for making the decisions about the filing of the document, such as how the filing is managed, what content the document includes, and when and where the filing occurs. The following three scenarios provide examples.

Scenario 1: Consider an attorney who completes a company creation document using information provided by a client, and then sends the document to a corporate service provider for filing with a secretary of state. In this example:

The attorney is the company applicant who is primarily responsible for directing or controlling the filing because they prepared the creation document and directed the corporate service provider to file it.

The individual at the corporate service provider is the company applicant who directly filed the document with the secretary of state.

Scenario 2: If the attorney instructs a paralegal to complete the preparation of the creation document, rather than doing so themself, before directing the corporate service provider to file the document, the outcome remains the same: the attorney and the individual at the corporate service provider who files the document are company applicants. The paralegal is not a company applicant because the attorney played a greater role than the paralegal in making substantive decisions about the filing of the document.

Scenario 3: If the client who initiated the company creation directly asks the corporate service provider to file the document to create the company, then the client is primarily responsible for directing or controlling the filing, and the client should be reported as a company applicant, along with the individual at the corporate service provider who files the document.

E. 6. Is a third-party courier or delivery service employee who only delivers documents that create or register a reporting company a company applicant?

No. A third-party courier or delivery service employee who only delivers documents to a secretary of state or similar office is not a company applicant provided they meet one condition: the third-party courier, the delivery service employee, and any delivery service that employs them does not play any other role in the creation or registration of the reporting company.

When a third-party courier or delivery service employee is used solely for delivery, the individual (e.g., at a business formation service or law firm) who requested the third-party courier or delivery service to deliver the document will typically be a company applicant.

Under FinCEN’s regulations, an individual who “directly files the document” that creates or registers the reporting company is a company applicant. Third-party couriers or delivery service employees who deliver such documents facilitate the documents’ filing, but FinCEN does not consider them to be the filers of the documents given their only connection to the creation or registration of the reporting company is couriering the documents.

Rather, when a third-party courier or delivery service is used by a firm, the company applicant who “directly files” the creation or registration document is the individual at the firm who requests that the third-party courier or delivery service deliver the documents.

For example, an attorney at a law firm may be involved in the preparation of incorporation documents. The attorney directs a paralegal to file the documents. The paralegal may then request a third-party delivery service to deliver the incorporation documents to the secretary of state’s office. The paralegal is the company applicant who directly files the documents, even though the third-party delivery service delivered the documents on the paralegal’s behalf. The attorney at the law firm who was involved in the preparation of the incorporation documents and who directed the paralegal to file the documents will also be a company applicant because the attorney was primarily responsible for directing or controlling the filing of the documents.

In contrast, if a courier is employed by a business formation service, law firm, or other entity that plays a role in the creation or registration of the reporting company, such as drafting the relevant documents or compiling information to be submitted as part of the documents delivered, the conclusion is different. FinCEN considers such a courier to have directly filed the documents—and thus to be a company applicant—given the courier’s greater connection (via the courier’s employer) to the creation or registration of the company.

For example, a mailroom employee at a law firm may physically deliver the document that creates a reporting company at the direction of an attorney at the law firm who is primarily responsible for decisions related to the filing. Both individuals are company applicants.

E. 7. If an individual used an automated incorporation service, such as through a website or online platform, to file the creation or registration document for a reporting company, who is the company applicant?

If a business formation service only provides software, online tools, or generally applicable written guidance that are used to file a creation or registration document for a reporting company, and employees of the business service are not directly involved in the filing of the document, the employees of such services are not company applicants. For example, an individual may prepare and self-file documents to create the individual’s own reporting company through an automated incorporation service. In this case, this reporting company reports only that individual as a company applicant.

F. 1. Will a reporting company need to report any other information in addition to information about its beneficial owners?

Yes. The information that needs to be reported, however, depends on when the company was created or registered.

If a reporting company is created or registered on or after January 1, 2024, the reporting company will need to report information about itself, its beneficial owners, and its company applicants.

If a reporting company was created or registered before January 1, 2024, the reporting company only needs to provide information about itself and its beneficial owners. The reporting company does not need to provide information about its company applicants.

F. 2. What information will a reporting company have to report about itself?

A reporting company will have to report:

Its legal name;

Any trade names, “doing business as” (d/b/a), or “trading as” (t/a) names;

The current street address of its principal place of business if that address is in the United States (for example, a U.S. reporting company’s headquarters), or, for reporting companies whose principal place of business is outside the United States, the current address from which the company conducts business in the United States (for example, a foreign reporting company’s U.S. headquarters);

Its jurisdiction of formation or registration; and

Its Taxpayer Identification Number (or, if a foreign reporting company has not been issued a TIN, a tax identification number issued by a foreign jurisdiction and the name of the jurisdiction).

A reporting company will also have to indicate whether it is filing an initial report, or a correction or an update of a prior report.

FinCEN’s Small Entity Compliance Guide includes a checklist to help identify the information required to be reported (see Chapter 4.1, “What information should I collect about my company, its beneficial owners, and its company applicants?”).

F. 3. What information will a reporting company have to report about its beneficial owners?

For each individual who is a beneficial owner, a reporting company will have to provide:

The individual’s name;

Date of birth;

Residential address; and

An identifying number from an acceptable identification document such as a passport or U.S. driver’s license, and the name of the issuing state or jurisdiction of identification document (for examples of acceptable identification, see Question F.5).

The reporting company will also have to report an image of the identification document used to obtain the identifying number in item 4.

FinCEN’s Small Entity Compliance Guide includes a checklist to help identify the information required to be reported (see Chapter 4.1, “What information should I collect about my company, its beneficial owners, and its company applicants?”).

F. 4. What information will a reporting company have to report about its company applicants?

For each individual who is a company applicant, a reporting company will have to provide:

The individual’s name;

Date of birth;

Address; and

An identifying number from an acceptable identification document such as a passport or U.S. driver’s license, and the name of the issuing state or jurisdiction of identification document (for examples of acceptable identification, see Question F.5).

The reporting company will also have to report an image of the identification document used to obtain the identifying number in item 4.

If the company applicant works in corporate formation—for example, as an attorney or corporate formation agent—then the reporting company must report the company applicant’s business address. Otherwise, the reporting company must report the company applicant’s residential address.

FinCEN’s Small Entity Compliance Guide includes a checklist to help identify the information required to be reported (see Chapter 4.1, “What information should I collect about my company, its beneficial owners, and its company applicants?”).

F. 5. What are some acceptable forms of identification that will meet the reporting requirement?

The only acceptable forms of identification are:

A non-expired U.S. driver’s license (including any driver’s licenses issued by a commonwealth, territory, or possession of the United States);

A non-expired identification document issued by a U.S. state or local government, or Indian Tribe;

A non-expired passport issued by the U.S. government; or

A non-expired passport issued by a foreign government (only when an individual does not have one of the other three forms of identification listed above).

F. 6. Is there a requirement to annually report beneficial ownership information?

No. There is no annual reporting requirement. Reporting companies must file an initial BOI report and updated or corrected BOI reports as needed.

FinCEN’s Small Entity Compliance Guide includes more information about when to file initial BOI reports in Chapter 5.1, “When should my company file its initial BOI report?” and when to file updated and corrected BOI reports in Chapter 6, “What if there are changes to or inaccuracies in reported information?”

F. 7. Does a reporting company have to report information about its parent or subsidiary companies?

No, though if a special reporting rule applies, the reporting company may report a parent company’s name instead of beneficial ownership information. A reporting company usually must report information about itself, its beneficial owners, and, for reporting companies created or registered on or after January 1, 2024, its company applicants. However, under a special reporting rule, a reporting company may report a parent company’s name in lieu of information about its beneficial owners if its beneficial owners only hold their ownership interest in the reporting company through the parent company and the parent company is an exempt entity.

Chapter 4 of FinCEN’s Small Entity Compliance Guide (“What specific information does my company need to report?”) provides additional information on what must be reported to FinCEN. Chapter 4.2 (“What do I report if a special reporting rule applies to my company?”) specifically provides details on what information must be reported pursuant to special reporting rules.

F. 8. Can a reporting company report a P.O. box as its current address?

No. The reporting company address must be a U.S. street address and cannot be a P.O. box.

FinCEN’s Small Entity Compliance Guide includes additional information on what must be reported in Chapter 4, “What specific information does my company need to report?”

F. 9. Have I met FinCEN’s BOI reporting obligation if I filed a form or report that provides beneficial ownership information to a state office, a financial institution, or the IRS?

No. Reporting companies must report beneficial ownership information directly to FinCEN. Congress enacted a law, the Corporate Transparency Act, that requires the reporting of beneficial ownership information directly to FinCEN. State or local governments, financial institutions, and other federal agencies, such as the IRS, may separately require entities to report certain beneficial ownership information. However, by law, those requirements are not a substitute for reporting beneficial ownership information to FinCEN.

F. 10. If a beneficial owner or company applicant’s acceptable identification document does not include a photograph for religious reasons, will FinCEN accept the identification document without the photograph?

Yes. If a beneficial owner or company applicant’s identification document does not include a photograph for religious reasons, the reporting company may nonetheless submit an image of that identification document when submitting its report, as long as the identification document is one of the types of identification accepted by FinCEN, such as a non-expired State-issued identification document. Please see Question F.5 for a list of acceptable identification documents.

F. 11. What residential address should be reported if a reporting company is required to a report an individual’s residential address, but that individual does not have a permanent residential residence?

The residential address that is current at the time of filing should be reported to FinCEN. An updated report should be submitted within 30 calendar days if the address, or any other information previously reported, changes.

FinCEN’s Small Entity Compliance Guide includes additional information on what information must be reported in Chapter 4, “What specific information does my company need to report?” and what to do when previously reported information needs to be updated in Chapter 6.1 “What should I do if previously reported information changes?”

G. 1. When do I have to file an initial beneficial ownership information report with FinCEN?

If your company existed before January 1, 2024, it must file its initial beneficial ownership information report by January 1, 2025.

If your company was created or registered on or after January 1, 2024, and before January 1, 2025, then it must file its initial beneficial ownership information report within 90 calendar days after receiving actual or public notice that its creation or registration is effective. Specifically, this 90-calendar day deadline runs from the time the company receives actual notice that its creation or registration is effective, or after a secretary of state or similar office first provides public notice of its creation or registration, whichever is earlier.

If your company was created or registered on or after January 1, 2025, it must file its initial beneficial ownership information report within 30 calendar days after receiving actual or public notice that its creation or registration is effective. The following sets out the initial report timelines. .

Chapter 5.1 “When should my company file its initial BOI report?” of FinCEN’s Small Entity Compliance Guide has additional information about the reporting timelines.

G. 3. How can I obtain a Taxpayer Identification Number (TIN) for a new company quickly so that I can file an initial beneficial ownership information report on time?

The Internal Revenue Service (IRS) offers a free online application for an Employer Identification Number (EIN), a type of TIN, which is provided immediately upon submission of the application. For more information on TINs, see “Taxpayer Identification Numbers (TIN)” at IRS.gov (https://www.irs.gov/individuals/international-taxpayers/taxpayer-identification-numbers-tin). For more information on Employer Identification Numbers and to access the EIN online application, see “Apply for an Employer Identification Number (EIN) Online” at IRS.gov (https://www.irs.gov/businesses/small-businesses-self-employed/apply-for-an-employer-identification-number-ein-online).

A paper filing is required if a foreign person that does not have an Individual Taxpayer Identification Number (ITIN) applies for an EIN. According to the IRS, receiving an EIN through this process could take six to eight weeks. If you are a foreign person that may need to obtain an EIN for a reporting company, we recommend applying early for an ITIN. Foreign reporting companies that are not subject to U.S. corporate income tax may report a foreign tax identification number and the name of the relevant jurisdiction instead of an EIN or TIN.

G. 4. Should an initial BOI report include historical beneficial owners of a reporting company, or only beneficial owners as of the time of filing?

An initial BOI report should only include the beneficial owners as of the time of the filing. Reporting companies should notify FinCEN of changes to beneficial owners and related BOI through updated reports.

FinCEN’s Small Entity Compliance Guide includes more information about when to file updated or corrected BOI reports in Chapter 6, “What if there are changes to or inaccuracies in reported information?”

G. 5. How does a company created or registered after January 1, 2024, determine its date of creation or registration?

The date of creation or registration for a reporting company is the earlier of the date on which: (1) the reporting company receives actual notice that its creation (or registration) has become effective; or (2) a secretary of state or similar office first provides public notice, such as through a publicly accessible registry, that the domestic reporting company has been created or the foreign reporting company has been registered.

FinCEN recognizes that there are varying state filing practices. In certain states, automated systems provide notice of creation or registration to newly created or registered companies. In other states, no actual notice of creation or registration is provided, and newly created companies receive notice through the public posting of state records. FinCEN believes that individuals who create or register reporting companies will likely stay apprised of creation or registration notices or publications, given those individuals’ interest in establishing an operating business or engaging in the activity for which the reporting company is created.

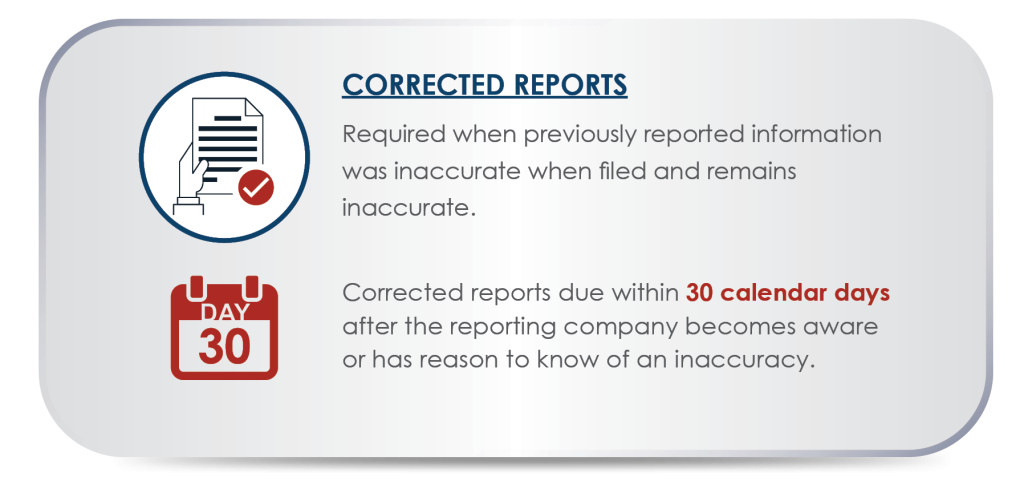

H. 1. What should I do if previously reported information changes?

If there is any change to the required information about your company or its beneficial owners in a beneficial ownership information report that your company filed, your company must file an updated report no later than 30 days after the date of the change.

A reporting company is not required to file an updated report for any changes to previously reported information about a company applicant.

The following infographic sets out updated reports timelines.

Chapter 6.1, “What should I do if previously reported information changes?” of FinCEN’s Small Entity Compliance Guide provides additional information.

H. 2. What are some likely triggers for needing to update a beneficial ownership information report?

The following are some examples of the changes that would require an updated beneficial ownership information report:

Any change to the information reported for the reporting company, such as registering a new business name.

A change in beneficial owners, such as a new CEO, or a sale that changes who meets the ownership interest threshold of 25 percent (see Question D.4 for more information about ownership interests).

Any change to a beneficial owner’s name, address, or unique identifying number previously provided to FinCEN. If a beneficial owner obtained a new driver’s license or other identifying document that includes a changed name, address, or identifying number, the reporting company also would have to file an updated beneficial ownership information report with FinCEN, including an image of the new identifying document.

FinCEN’s Small Entity Compliance Guide provides additional guidance on triggers requiring an updated beneficial ownership information report (see Chapter 6.1 “What should I do if previously reported information changes?”).

H. 3. Is an updated BOI report required when the type of ownership interest a beneficial owner has in a reporting company changes?

No. A change to the type of ownership interest a beneficial owner has in a reporting company—for example, a conversion of preferred shares to common stock—does not require the reporting company to file an updated BOI report because FinCEN does not require companies to report the type of interest. Updated BOI reports are required when information reported to FinCEN about the reporting company or its beneficial owners changes.

FinCEN’s Small Entity Compliance Guide includes additional information on when and how reporting companies must update information in Chapter 6, “What if there are changes to or inaccuracies in reported information?”

H. 4. If a reporting company needs to update one piece of information on a BOI report, such as its legal name, does the reporting company have to fill out an entire new BOI report?

Updated BOI reports will require all fields to be submitted, including the updated pieces of information. For example, if a reporting company changes its legal name, the reporting company will need to file an updated BOI report to include the new legal name and the previously reported, unchanged information about the company, its beneficial owners, and, if required, its company applicants.

A reporting company that filed its prior BOI report using the fillable PDF version may update its saved copy and resubmit to FinCEN. If a reporting company used FinCEN’s web-based application to submit the previous BOI report, it will need to submit a new report in its entirety by either accessing FinCEN’s web-based application to complete and file the BOI report, or by using the PDF option to complete the BOI report and upload to the BOI e-Filing application.

H. 5. Can a filer submit a late updated BOI report?

An updated BOI report can be submitted to FinCEN at any time. However, the reporting company is responsible for ensuring that updates are filed within 30 days of a change occurring. If a reporting company has engaged a third-party service provider to file BOI reports and updates on its behalf, then it should communicate any changes to its beneficial ownership information to the third-party service provider with enough time to meet the 30-day deadline.

H. 6. If a reporting company last filed a “newly exempt entity” BOI report but subsequently loses its exempt status, what should it do?

A reporting company should file an updated BOI report with FinCEN with the company’s current beneficial ownership information when it determines it no longer qualifies for an exemption.

I. 1. What should I do if I learn of an inaccuracy in a report?

If a beneficial ownership information report is inaccurate, your company must correct it no later than 30 days after the date your company became aware of the inaccuracy or had reason to know of it. This includes any inaccuracy in the required information provided about your company, its beneficial owners, or its company applicants. The following infographic sets out the corrected report timelines.

Chapter 6.2, “What should I do if I learn of an inaccuracy in a report?” of FinCEN’s Small Entity Compliance Guide includes additional information about correcting inaccurate beneficial ownership information reports filed with FinCEN.

J. 1. What should a reporting company do if it becomes exempt after already filing a report?

If a reporting company filed a beneficial ownership information report but then becomes exempt from filing the report, the company should file an updated report indicating that it is no longer a reporting company. An updated BOI report for a newly exempt entity will only require that: (1) the entity identify itself; and (2) check a box noting its newly exempt status. Chapter 6.3, “What should my company do if it becomes exempt after already filing a report?” of FinCEN’s Small Entity Compliance Guide includes more information.

K. 1. What happens if a reporting company does not report beneficial ownership information to FinCEN or fails to update or correct the information within the required timeframe?

FinCEN is working hard to ensure that reporting companies are aware of their obligations to report, update, and correct beneficial ownership information. FinCEN understands this is a new requirement. If you correct a mistake or omission within 90 days of the deadline for the original report, you may avoid being penalized. However, you could face civil and criminal penalties if you disregard your beneficial ownership information reporting obligations.

FinCEN’s Small Entity Compliance Guide provides more information about enforcement of the requirement (see Chapter 1.3, “What happens if my company does not report BOI in the required timeframe?”).

K. 2. What penalties do individuals face for violating BOI reporting requirements?

As specified in the Corporate Transparency Act, a person who willfully violates the BOI reporting requirements may be subject to civil penalties of up to $500 for each day that the violation continues. That person may also be subject to criminal penalties of up to two years imprisonment and a fine of up to $10,000. Potential violations include willfully failing to file a beneficial ownership information report, willfully filing false beneficial ownership information, or willfully failing to correct or update previously reported beneficial ownership information.

K. 3. Who can be held liable for violating BOI reporting requirements?

Both individuals and corporate entities can be held liable for willful violations. This can include not only an individual who actually files (or attempts to file) false information with FinCEN, but also anyone who willfully provides the filer with false information to report. Both individuals and corporate entities may also be liable for willfully failing to report complete or updated beneficial ownership information; in such circumstances, individuals can be held liable if they either cause the failure or are a senior officer at the company at the time of the failure.

i. Can an individual who files a report on behalf of a reporting company be held liable?

Yes. An individual who willfully files a false or fraudulent beneficial ownership information report on a company’s behalf may be subject to the same civil and criminal penalties as the reporting company and its senior officers.

ii. Can a beneficial owner or company applicant be held liable for refusing to provide required information to a reporting company?

Yes. As described above, an enforcement action can be brought against an individual who willfully causes a reporting company’s failure to submit complete or updated beneficial ownership information to FinCEN. This would include a beneficial owner or company applicant who willfully fails to provide required information to a reporting company.

K. 4. Is a reporting company responsible for ensuring the accuracy of the information that it reports to FinCEN, even if the reporting company obtains that information from another party?

Yes. It is the responsibility of the reporting company to identify its beneficial owners and company applicants, and to report those individuals to FinCEN. At the time the filing is made, each reporting company is required to certify that its report or application is true, correct, and complete. Accordingly, FinCEN expects that reporting companies will take care to verify the information they receive from their beneficial owners and company applicants before reporting it to FinCEN.

K. 5. What should a reporting company do if a beneficial owner or company applicant withholds information?

While FinCEN recognizes that much of the information required to be reported about beneficial owners and company applicants will be provided to reporting companies by those individuals, reporting companies are responsible for ensuring that they submit complete and accurate beneficial ownership information to FinCEN. Starting January 1, 2024, reporting companies will have a legal requirement to report beneficial ownership information to FinCEN.

Existing reporting companies should engage with their beneficial owners to advise them of this requirement, obtain required information, and revise or consider putting in place mechanisms to ensure that beneficial owners will keep reporting companies apprised of changes in reported information, if necessary. Beneficial owners and company applicants should also be aware that they may face penalties if they willfully cause a reporting company to fail to report complete or updated beneficial ownership information.

Persons considering creating or registering legal entities that will be reporting companies should take steps to ensure that they have access to the beneficial ownership information required to be reported to FinCEN, and that they have mechanisms in place to ensure that the reporting company is kept apprised of changes in that information.

L. 1. What are the criteria for the tax-exempt entity exemption from the beneficial ownership information reporting requirement?

An entity qualifies for the tax-exempt entity exemption if any of the following four criteria apply:

(1) The entity is an organization that is described in section 501(c) of the Internal Revenue Code of 1986 (Code) (determined without regard to section 508(a) of the Code) and exempt from tax under section 501(a) of the Code.

(2) The entity is an organization that is described in section 501(c) of the Code, and was exempt from tax under section 501(a) of the Code, but lost its tax-exempt status less than 180 days ago.

(3) The entity is a political organization, as defined in section 527(e)(1) of the Code, that is exempt from tax under section 527(a) of the Code.

(4) The entity is a trust described in paragraph (1) or (2) of section 4947(a) of the Code.

FinCEN’s Small Entity Compliance Guide includes checklists for this exemption (see exemption #19) and for the additional exemptions to the reporting requirements (see Chapter 1.2, “Is my company exempt from the reporting requirements?”).

L. 2. What are the criteria for the inactive entity exemption from the beneficial ownership information reporting requirement?

An entity qualifies for the inactive entity exemption if all six of the following criteria apply:

(1) The entity was in existence on or before January 1, 2020.

(2) The entity is not engaged in active business.

(3) The entity is not owned by a foreign person, whether directly or indirectly, wholly or partially. “Foreign person” means a person who is not a United States person. A United States person is defined in section 7701(a)(30) of the Internal Revenue Code of 1986 as a citizen or resident of the United States, domestic partnership and corporation, and other estates and trusts.

(4) The entity has not experienced any change in ownership in the preceding twelve-month period.

(5) The entity has not sent or received any funds in an amount greater than $1,000, either directly or through any financial account in which the entity or any affiliate of the entity had an interest, in the preceding twelve-month period.

(6) The entity does not otherwise hold any kind or type of assets, whether in the United States or abroad, including any ownership interest in any corporation, limited liability company, or other similar entity.

FinCEN’s Small Entity Compliance Guide includes checklists for this exemption (see exemption #23) and for the additional exemptions to the reporting requirements (see Chapter 1.2, “Is my company exempt from the reporting requirements?”).

L. 3. What are the criteria for the subsidiary exemption from the beneficial ownership information reporting requirement?

Subsidiaries of certain types of entities that are exempt from the beneficial ownership information reporting requirements may also be exempt from the reporting requirement.

An entity qualifies for the subsidiary exemption if the following applies:

The entity’s ownership interests are controlled or wholly owned, directly or indirectly, by any of these types of exempt entities:

Securities reporting issuer;

Governmental authority;

Bank;

Credit union;

Depository institution holding company;

Broker or dealer in securities;

Securities exchange or clearing agency;

Other Exchange Act registered entity;

Investment company or investment adviser;

Venture capital fund adviser;

Insurance company;

State-licensed insurance producer;

Commodity Exchange Act registered entity;

Accounting firm;

Public utility;

Financial market utility;

Tax-exempt entity; or

Large operating company.

FinCEN’s Small Entity Compliance Guide includes definitions of the exempt entities listed above and a checklist for this exemption (see exemption #22). FinCEN’s Guide also includes checklists for the additional exemptions to the reporting requirements (see Chapter 1.2, “Is my company exempt from the reporting requirements?”).

L. 4. If I own a group of related companies, can I consolidate employees across those companies to meet the criteria of a large operating company exemption from the reporting company definition?

No. The large operating company exemption requires that the entity itself employ more than 20 full-time employees in the United States and does not permit consolidation of this employee count across multiple entities.

L. 5. How does a company report to FinCEN that the company is exempt?

A company does not need to report to FinCEN that it is exempt from the BOI reporting requirements if it has always been exempt.

If a company filed a BOI report and later qualifies for an exemption, that company should file an updated BOI report to indicate that it is newly exempt from the reporting requirements. Updated BOI reports are filed electronically though the secure filing system. An updated BOI report for a newly exempt entity will only require that the entity: (1) identify itself; and (2) check a box noting its newly exempt status.

L. 6. Does a subsidiary whose ownership interests are partially controlled by an exempt entity qualify for the subsidiary exemption?

No. If an exempt entity controls some but not all of the ownership interests of the subsidiary, the subsidiary does not qualify. To qualify, a subsidiary’s ownership interests must be fully, 100 percent owned or controlled by an exempt entity.

A subsidiary whose ownership interests are controlled or wholly owned, directly or indirectly, by certain exempt entities is exempt from the BOI reporting requirements. In this context, control of ownership interests means that the exempt entity entirely controls all of the ownership interests in the reporting company, in the same way that an exempt entity must wholly own all of a subsidiary’s ownership interests for the exemption to apply.

A “FinCEN identifier” is a unique identifying number that FinCEN will issue to an individual or reporting company upon request after the individual or reporting company provides certain information to FinCEN. An individual or reporting company may only receive one FinCEN identifier.

FinCEN’s Small Entity Compliance Guide includes additional information on FinCEN identifiers in Chapter 4.3, “What is a FinCEN identifier and how can I use it?”

When a beneficial owner or company applicant has obtained a FinCEN identifier, reporting companies may report the FinCEN identifier of that individual in the place of that individual’s otherwise required personal information on a beneficial ownership information report.

A reporting company may report another entity’s FinCEN identifier and full legal name in place of information about its beneficial owners when three conditions are met: (1) the other entity obtains a FinCEN identifier and provides it to the reporting company; (2) the beneficial owners hold interests in the reporting company through ownership interests in the other entity; and (3) the beneficial owners of the reporting company and the other entity are the exact same individuals.

Individuals may request a FinCEN identifier starting January 1, 2024, by completing an electronic web form at https://fincenid.fincen.gov. Individuals will need to provide their full legal name, date of birth, address, unique identifying number and issuing jurisdiction from an acceptable identification document, and an image of the identification document. After an individual submits this information, they will immediately receive a unique FinCEN identifier.

Reporting companies may request a FinCEN identifier by checking a box on the beneficial ownership information report upon submission. After the reporting company submits the report, the company will immediately receive a unique FinCEN identifier. If a reporting company wishes to request a FinCEN identifier after submitting its initial beneficial ownership report, it may submit an updated beneficial ownership information report requesting a FinCEN identifier, even if the company does not otherwise need to update its information.

M. 5. Do I need to update or correct the information I submitted to obtain a FinCEN identifier?

Yes. Individuals must update or correct information through the FinCEN identifier application that is also used to request a FinCEN identifier.

Individuals must report any change to the information they submitted to obtain a FinCEN identifier no later than 30 days after the date on which the change occurred.

If there is any inaccuracy in this information, an individual must correct the information no later than 30 days after the date the individual became aware of the inaccuracy or had reason to know of it.

Reporting companies with a FinCEN identifier must update or correct the company’s information by filing an updated or corrected beneficial ownership information report, as appropriate.

M. 6. Is there any way to deactivate an individual’s FinCEN identifier that is no longer in use so that the individual no longer has to update the information associated with it?

FinCEN is actively assessing options to allow individuals to deactivate a FinCEN identifier so that they do not need to update the underlying personal information on an ongoing basis. FinCEN will provide additional guidance on this functionality upon completion of that process.

M. 7. Who can request a FinCEN identifier on behalf of an individual?

Anyone authorized to act on behalf of an individual may request a FinCEN identifier on the individual’s behalf on or after January 1, 2024.