Author: Published: 6/1/2023 Solar Power World

Climate change is driving an urgent shift to renewable energy — arguably one of the biggest opportunities of our generation — and insurance is playing a critical role. Just a few years ago, insurance was a “check the box” in renewable energy project financing — a small and easily dealt with detail that renewable asset owners completed upon starting a project. Today, it has become an essential part of the project finance puzzle. If an asset is uninsurable, it is unfinanceable. And yet insurance continues to be an enigma in the renewable energy industry.

Renewable energy insurance 101

To understand the insurance challenges renewable energy sponsors face, it’s important to understand the insurance space and the pivotal role it plays in financing and protecting renewable assets.

To understand the insurance challenges renewable energy sponsors face, it’s important to understand the insurance space and the pivotal role it plays in financing and protecting renewable assets.

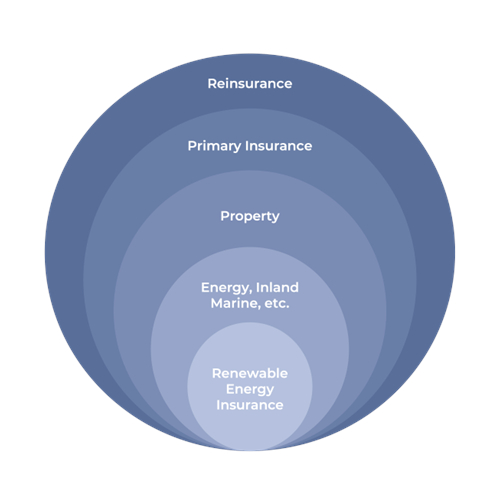

In the value chain, insurance usually flows from the project sponsor or asset manager, through the brokers, and then finally to the insurance carrier. Specialty products like solar and wind energy often involve managing general agents (MGAs), who specialize in the asset class and help carriers understand and underwrite risk.

Renewable energy insurance is impacted by the entire (re)insurance ecosystem; it typically sits within a carrier’s energy/inland marine book, which is within a property insurance book. The carrier then purchases reinsurance across multiple lines of business to insulate against risks from a large claim — essentially insurance for the insurance companies.

Challenges

Although opportunities abound in the renewable industry, rapid, massive growth does not come without challenges for insurers. And a retreat by insurers ultimately impacts project financing for renewable providers.

Skyrocketing reinsurance rates

Reinsurance typically renews on January 1, and this year’s renewals proved to be especially difficult. Significant natural catastrophe losses in past years resulted in skyrocketing reinsurance rates across many insurance types, particularly for natural catastrophe coverage. And clients and sponsors are feeling the effects in all lines of business, including renewables.

Lack of renewable underwriting expertise

Since renewable energy is still a newer asset class, there are few underwriters and agencies with the expertise and specialization to truly understand the nuances and risks associated with solar panels, wind turbines and storage. As a very specialized asset class experiencing massive growth, working with an insurer who has renewable experience could be the deciding factor in whether a project receives critical financing. Underwriters should be looking at attritional risks, such as the chance of inverter failure, vandalism, etc., as well as natural catastrophe risks like winter storm, wind, hurricane, earthquake, fire, flood and relying on weather-adjusted performance data to drive decisions.

Increased natural catastrophe losses

Natural catastrophe risks receive a lot of attention, and for good reason — such events have tripled in frequency over the past 50 years. These shocks to the system have caused the industry, and carriers in particular, significant concern when managing renewable energy. Major hail and hurricane events have resulted in outsized losses in carriers’ books, which are now passed onto end customers through higher premiums and tighter terms and conditions.

Impact on renewable financing

Pre-2019, insurance was abundant and asset owners and renewable sponsors could receive as much as they asked for. Between 2019 and 2022, outsized natural catastrophe losses catalyzed changing insurance terms, driving up premiums and driving down capacity, creating a difficult environment for insureds. This has not only impacted existing renewable asset owners, but it also had dramatic repercussions on financing for new renewable projects.

Using innovation to control risks

Swift Current project in Illinois. Credit: Rich Saal/Swift Current Energy

Today, risk allocation is rapidly shifting, placing the onus on asset owners to demonstrate resiliency — and that costs money. The good news is that there is a lot of innovation in renewable energy, particularly around data and resiliency. With more and better data entering the space, modeling and pricing have become more accurate. Being able to understand weather predictions, the frequency of natural catastrophe events and the actual outcomes on assets when such events occur is key. Today, we’re having conversations about correct hail stow angles and vegetation management, topics that were not nearly as active even five years ago.

Looking ahead, the key will be continued innovation and the further adoption of resilient practices. Sponsors can control some of their risk by diversifying their portfolio geographically and ensuring that adequate operations and management protocols are in place for their sites. Insurance has become a crucial part of the development process and it’s important to understand it in a global context. Working with knowledgeable, specialized and data-driven carriers will help unlock this lucrative form of capital for the renewable energy industry.